Benefits of Developing an Internal Accounting Structure

By Emanuel Schwarz

Aug. 24, 1998 (Pro2Net) If you had opportunity to read my first article, "Why You Need an Internal Accounting Structure," you have surely received the clear impression, that we, who are working with industrial accounting, should accept the absolute need to develop a specific internal accounting structure.

![]()

Most of us have read articles and books about the importance of separating the financial accounting structure (the external chart of accounts), from the internal accounting structure. This should have a special chart of accounts that will adjust to the basic requirements of managers who need information regarding the internal budgeting and control of their company.

But a company should have one chart of accounts that covers both the external and the internal needs.

Today, the chart of accounts includes only the expense accounts that a company must have in accordance to GAAP. If we separate the external transactions from the internal one, we will be able to start the internal chart of accounts, with accounts that only refer to accrued expenses.

This group of accrued values would also include accounts that the GAAP does not currently accept. We refer to such accounts as the interest values referring to our investments.

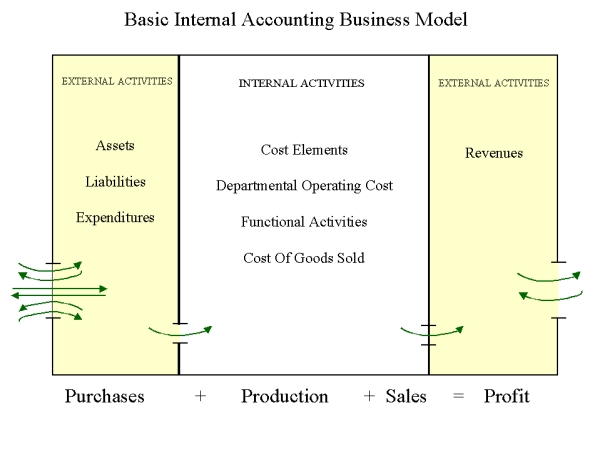

This graphic demonstrates the activity of purchases plus the activity of production and sales results in profit:

With this new approach we professionals and teachers can begin to use more appropriate terminology. For example, we can use "cost" only for our internal transactions. We can now clean up present terminology such as "cost of goods sold."

As the terminology now is established, we should refer to these accounts as "expenses of cost of goods sold." We no longer need to use an irrational combination of expense and cost.

Today a similar problem exists with terms such as "direct," "indirect," "fixed" and "variable cost." We only use the term of "cost" -- nothing referring to expense.

So why not call values (transactions of any kind) within internal accounting "cost"?

Consider the following two graphics.

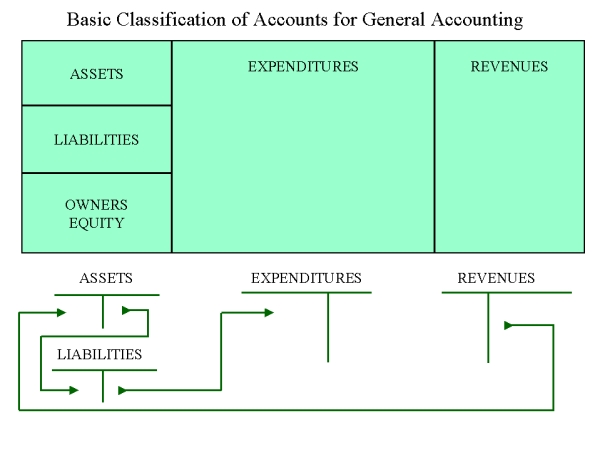

Exhibit 1-6

The correct terminology is important for our modern accounting structure; however the most favorable benefit that management will receive is the totally new approach to structure a chart of accounts, specifically for the internal managerial needs.

Analyze Exhibit 1-6 to see how financial accounting is arranged only to serve external needs of a company. This financial structure was developed some 70 to 80 years ago - and up to this day we keep this chart because it follows perfectly well the instructions we have from GAAP.

The larger auditing companies have not developed any chart related to internal accounting: It would cost them too much money to educate their staff to understand the true nature of cost accounting. The CEOs of these companies are therefore in part responsible for the fact that we still have only one overhead account in a company with several direct production departments and that these companies are using only one absorption rate for all indirect cost charged to the different products.

This is an absolutely unacceptable approach for internal information.

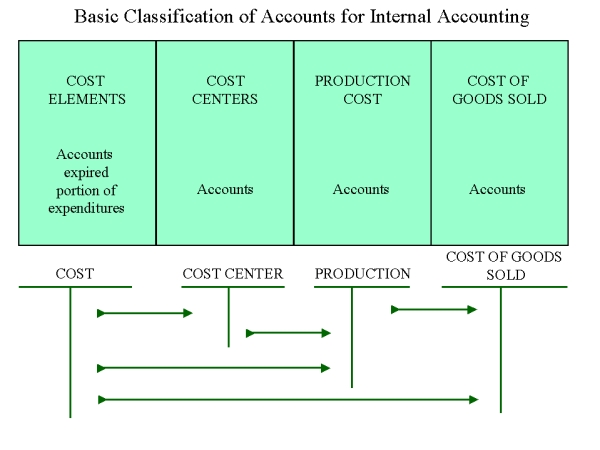

Exhibit 1-7 has the new and logical configuration that have been developed for internal accounting.

Exhibit 1-7

The internal chart of accounts starts with the cost elements - these are "the expired portion of expense" that correspond toward the production cost and any activity of this accounting period. We credit these cost element accounts with all the amounts that belong to this period.

These cost elements will be identified into three groups:

- Indirect Cost - will be charged to the different cost centers of a company: administrative, Direct and indirect production, and service departments.

- Direct Cost - will be charged directly to the functional activity accounts: production cost, maintenance and repair cost, and internal production.

- Cost of Goods Sold - these are the production, administrative and sales costs.

Also observe that Exhibit 1-7 includes transaction arrows that show the absorption cost taken to the functional activities and the transfer of finished goods values to the corresponding inventory accounts.

This Exhibit 1-7 is the most important graphic, as it explains how internal accounting should be developed.