Purpose of Internal Accounting

Analysis Made for the Internal Accounting Configuration

By: Emanuel Schwarz

Feb. 28, 2000 (Pro2Net) — Past articles have examined the importance of creating a specific Internal Accounting structure. This refers not only to establishing a few accounts with their subsidiary accounts, but to produce a whole new Chart of Accounts related strictly to the information needs expressed by management interested in good internal managerial reports.

![]()

General Accounting was created some 60 to 70 years ago and has always referred essentially to the needs of Financial and External Accounting. This financial structure is perfect for external users of the company - those who are interested in the economic entity. Therefore it can be said that External Accounting was never defined as an internal cost related accounting system.

As a consequence of this reality, CPAs and auditing companies have during the last 50 years shown little if any interest in helping manufacturing industries in their need to create an adequate Internal accounting structure.

The terminology in Financial Accounting is still totally inadequate. Terms such as "overhead accounts" and "work in process inventory accounts" were created by general accountants just to include in the Financial Accounting's frame some terminology that would refer to an Internal Accounting structure.

Financial Accountants said these few subsidiary accounts would be good enough for managerial information. Unfortunately, these statements were not at all correct.

In addition, university professors were not prepared to create during the last 30 years a real Internal Accounting structure. Stanford University's cost accounting books still show, in their latest versions, the same graphics of cost accounting transactions as they did it some 20 years ago. This same problem exists in other well-known universities across the United States.

These criticisms are not mine alone. There are other professionals that agree about the need to have a specific Chart of Accounts for Internal Accounting… many voices calling for an important change in accounting education and a professional approach to Internal Accounting.

James A. Brimson and Callie Berliner

CMA-I, Arlington, Texas:

"Management Accounting", March 1988:

"We believe that the authors of 'In Defense of Management Accounting' did an extremely poor job of supporting their thesis that management accounting does not need to undergo major changes. They present a naive belief that management accounting is practiced according to the broad definitions on which the article dwells. This is contrary to our experience. The dissatisfaction with current management accounting systems is evidenced by:

| Cost management seminars which are sold out months in advance. | |

| A 1986 CMA-I survey which found that 62 % of the respondents were dissatisfied with cost reporting." |

Robert S. Kaplan

Professor at Harvard University

In his article: "Yesterday's Accounting Undermines Production"

"Efforts to revitalize manufacturing industries cannot succeed if

outdated accounting and control systems remain unchanged. Many U.S.

companies are now exploiting new process technologies… but these

developments, promising as they are, rest on a foundation that is obsolete

and in need of repair. Most accounting and control system have major

problems: they distort product costs, they do not produce the key non

financial data required for effective and efficient operations; and the data

they do produce reflect external reporting requirements far more than they

do the reality of the new manufacturing environment. Most companies still

use the same cost accounting and management control system that were

developed decades ago for a competitive environment drastically different

from that of today."

Robert S. Kaplan

Professor at Harvard University

In his article " One Cost System is not Enough"

Harvard Business Review, January 1988

"Are managers getting the information they need to value inventory, control operations and measure product costs? Many companies now recognize that their cost systems are inadequate for today's powerful competition. Systems designed mainly to value inventory for financial and tax statements are not giving managers the accurate and timely information they need to promote operating efficiencies and measure product costs."

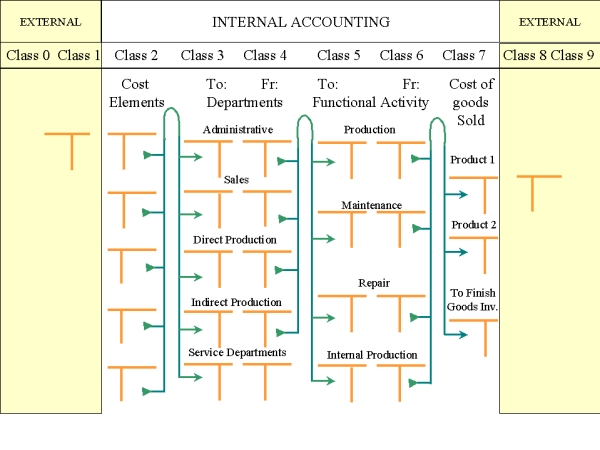

Developing an Internal Accounting Structure

To develop an Internal Accounting structure, a specific Chart of Accounts

should be created for this purpose. External Accounting should remain as it

is, with accounts related to Assets, Liabilities, Capital, Expense and

Revenue.

Internal Accounting would need to start with the expired amounts of the expense, that is the amounts that correspond to the functional activities of an accounting period and that also could be identified with the matching system of accounting teaching.

This first Classification of accounts would be called Cost Elements and will include all accounts needed for Direct Cost and Indirect Costs.

Once these Cost Elements are established, Direct Cost will be allocated to specific accounts in Class 5: To: Production Cost. All other Cost Elements will be identified as Indirect Costs and allocated to the different departments where they correspond.

Through this procedure, accounts referring to the Responsibility Accounting System will be included in Class 3. From Class 4, the operating cost of the direct production departments will be absorbed by the production realized during this time period.

These departmental operating costs will be charged to the different production accounts in Class 5. The finished production will be transferred from Class 6 to Inventory accounts in Class 7.