Reallocation of Departmental Operating Costs

An Analysis of the Internal Accounting Configuration

By Emanuel F. Schwarz

(May 10, 1999) - As in previous months, this article refers to the internal accounting of a hypothetical company.

This month, we will focus on the account that traditional accounting professors refer to as "overhead."![]()

As Stanford University's Professor Horngren noted in one of his cost accounting books, why did the professionals not call this account "underfoot"? In other words, Horngren accepted the need to change this unhappy denomination of "overhead" to some term more appropriate to the realities of our companies.

These accounts refer to the different departments (or cost centers) that we have. In other words, let us unquestionably change this unhappy term to "departments."

In my article published in April, I showed my readers how we should structure Class 3 of our internal accounting. I identified this class as: TO Departments. This means that we allocate our indirect cost elements to these departments.

I prefer to record the Administrative and Sales Departments in the beginning of Class 3. Once we have debited these indirect costs to the different departments, we must analyze how these departmental operating costs refer to, and should be applied to, our final Cost Objective, that is, our Production Cost.

We know that the Administrative and Sales Departments should not apply their operating costs to the production. These administrative and sales operating costs should be applied to the Cost of Goods Sold.

Then we have the Direct Production Departments, where the actual production is realized.

Consequently, these departmental operating costs must be applied to the production cost

account. We may also express it in following way: The products have to absorb these

departmental operating costs. -

But first let us analyze the operating costs of the following departments: Indirect Production and Service.

The Indirect Production departments, such as Quality Control, Maintenance or Repair, are working for, and helping to realize, production. But they are not working directly with our production and therefore we cannot charge to the Production Cost such operating costs as maintenance and repair of the machines. We also would not have any clear relationship of this activity cost toward the different products created.

So we need to structure the Reallocation steps, taking the operating cost of our Indirect Production and Service departments to the Direct Production departments. This Reallocation procedure is a very important step in developing an advanced managerial accounting.

In Activity Based Costing projections and teachings often discuss the need for Reallocation. ABC strongly indicates that we have to charge to the Production Cost account not only the direct related costs of the production but also costs accumulated in different departments that work in some indirect way with our production.

I refer to the Indirect Production departments, such as maintenance and repair. These Departmental Operating Costs must be absorbed by the products. We will not directly transfer these costs from credit Class 4 to debit Class 5, but instead take these costs as a reallocation amount from Class 4 back to Class 3: to the departments that use the service of these indirect departments.

With this procedure, we increase the total Departmental Operating Cost of the Direct Production Departments and, consequently, the Application Rate will also be increased in these departments. This means that when we multiply this pre-established rate times the production volume, we have then charged to the production not only the operating cost of the Direct Production Department but also the operating costs of these other Indirect and Service Departments.

With this procedure we are fulfilling instructions recommended by ABC.

Reallocation Procedure

Allow me to clarify that we must reallocate the operating costs of the Indirect and Service departments not only to the Direct Production departments but also to all other departments in our company that are receiving these different services. The Maintenance and Repair work may also have been realized in some Administrative or Sales department. So the whole question of reallocation is a serious and important procedure.

The responsible person for each department of the company will have to prepare their specific expenditure budget for the fiscal year and calculate the monthly average amount.

Budgeted Procedure

Once we have established the average monthly operating cost of the different Indirect and Service departments, we must calculate how much of these operating costs will be charged to the different receiving departments. This established dollar amount will be the reallocated value that we will transfer each month to the receiving departments.

This monthly amount will be used during the whole fiscal year, however, if special new conditions arise, we may change these monthly amounts. At the end of each year we should verify if these budgeted amounts are still acceptable or should be changed. We should not reallocate monthly the actual operating cost, but the pre-established budgeted amount.

Details of Reallocation

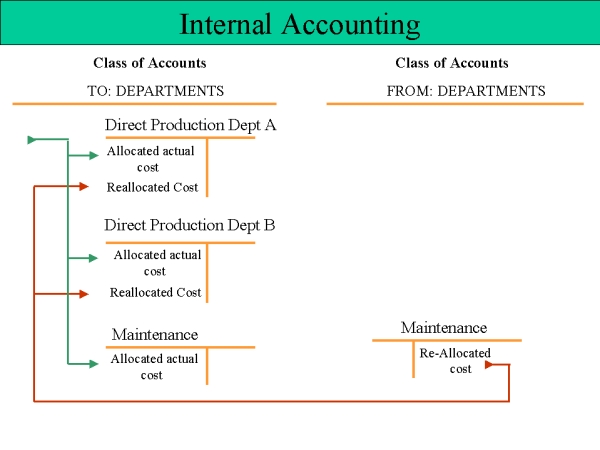

Note that the graphic includes a reallocation line that is leaving a Direct Production department. On the credit side of this account is written "Reallocate Service." The problem is: the Direct Production departments may have an office of the engineer in charge of these departments. The operating cost of this office must be reallocated to the different departments that the engineer is in charge of. Here again is the question of following the ABC indications.

The Graphic

In our internal accounting, we have the Responsibility Centers recorded under Class 3. These accounts will be debited with the actual operating cost of the month. There is a line coming from Class 2 and moving along the debit side of the accounts of Class 3. Then we see the reallocation line moving from the credit side of the Class 4 accounts, first down then to the left and finally up along the debit side of the accounts in Class 3.

Another line is leaving the credit side of the Class 4 accounts. This is the line that the applied amounts will use to be charged to the different Production Cost accounts in Class 5.

From the Administrative and Sales departments--that is, Class 4--the departmental operating costs will be applied to the Cost of Goods Sold, which will be discussed in future articles.

Conclusion You may now understand why I believe the phrase "overhead" is totally unacceptable for a managerial accounting structure. The overhead account was created by accountants during a time when it was not understood how important are the central points of the Responsibility Accounting System.