An Analysis Made for the Internal Accounting Configuration

By: Emanuel Schwarz

(January 31, 2000) - The implementation of Internal Accounting into companies and the structuring of a new Chart of Accounts for is the topic of much discussion and debate. If you are interested in past articles on this topic, they are available in the archives of the Pro2Net Web site.

![]()

This article again emphasizes the need of establishing specific accounts for the internal use of management, and will prepare you

to implement in your manufacturing company a new and modern

method of Internal Lease Transactions.

It is necessary to apply the cost of the machine used for any productive activity to the production cost of that product. In addition,

the Matching Principle must be followed - a specific production job order must be charged only the amount of the machine cost that

corresponds to it. How to do that is a difficult question.

For such a purpose, there is a method of determining the depreciation on the purchase cost of a

machine. This cost may be expressed either per calendar month, or per machine hour. The

depreciation cost per machine hour is a good measurement of the machine cost that should be applied to the product.

The production controlled by a job order will absorb the corresponding depreciation correctly, but there is

a problem. The operating cost per hour of the machine refers to more than just the depreciation of the

purchase value. There are other cost elements related to the operation of a machine, including:

|

The electricity or power needed for the machine to work | |

|

Insurance on the machine in case of loss. | |

|

The value of the space occupied by the machine . | |

|

Maintenance and repair on the machine . | |

|

The interest cost of capital invested |

Essentially, This list, shows the need to structure some type of basic cost system to determine how much a

machine actually costs per hour of its production time.

It is not difficult to establish how much electric power will cost per machine hour. The amount of insurance

per month can be converted to find the insurance cost per hour of production. The same can be done with

the space that the machine will occupy. Determine the square footage the machine will occupy, as well as

working space and rental costs for this type of building.

The cost of maintenance and repair on the machine is highly important, but more difficult to establish. The

first step is to establish the number of years the machine will be used in the company. Then, an estimate

must be made: how often must the machine be maintained and how much time

and material will be included in its maintenance. Maintenance can also be classified as daily,

weekly, monthly, etc. With these estimates, a dollar amount can be calculated for each year the machine is

working.

This is not an easy question, especially for a company with little experience with a particular machine. The

supplier may be able to assist in these estimations.

In same way the cost of repair of this machine must be assumed. Then, the maintenance and repair

amounts must be converted to an amount per production hour of the machine.

Finally the capital invested in this machine must be taken into account. When all these costs are

combined, the result is a realistic estimate of how much a machine will cost per hour of productive work.

With this knowledge it is possible to prepare an adequate accounting transaction model to be used with

any Internal Lease project. These accounting transactions correspond only to the Internal Accounting

structure rather than External (Financial) Accounting.

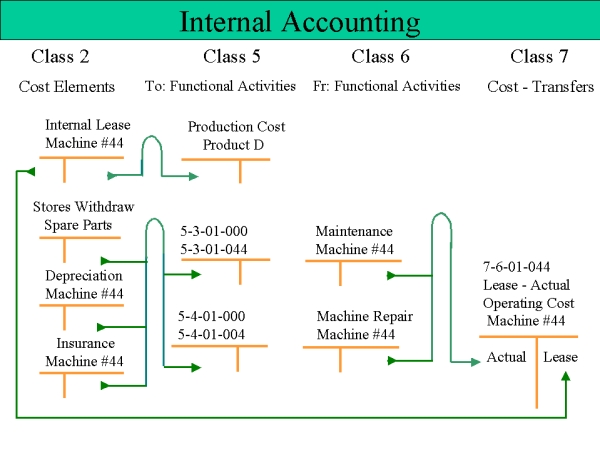

This diagram illustrates the above points, and again emphasizes how important it is to separate

Internal Accounting from External.

These transactions are created from Class 2 - Cost Elements. A Main Account is opened that we will call

Internal Lease. This account can be created in Group 3 accounts and would correspond to Store

Withdrawal. The Main Account could also be opened in Group 4.

The specific machine must be identified as a sub-account - in our example Machine #44. This sub-account

will be credited with the lease value that must be charged to Production Cost in Class 5 - and identify the

product and corresponding Job Order.

This transaction from Class 2 Internal Lease - Machine # 44 - will always be used when it is indicated that

Machine # 44 worked so many hours for the production of this Job Order. This means that the account of

this Job Order will be charged the amount of the pre-calculated lease cost

multiplied by the amount of hours worked.

Next the actual cost of maintaining and repairing this machine must be evaluated. In Class 2 is a Group of

Accounts referring to Store Withdrawal. All Spare Parts used in the company will be credited to the Main

Account. In addition to being credited to the Main account, any Spare Part that will be used to maintain

Machine #44, will be debited a corresponding account in Class 5-3-01-044, which was created to accumulate

all maintenance amounts for this machine.

At the end of each month, the amounts recorded in Class 5 will be credited the same amounts in Class 6-3-01-044 or 6-4-01-04 and transferred to Class 7. Here we have opened a

special account to show any

difference between the calculated lease amounts and the actual cost for the

month.