![]()

![]()

![]()

![]()

![]()

![]()

|

|

INTERNAL ACCOUNTING ENGINEERINGStructure and DevelopmentINTERNAL CHART OF ACCOUNTS .This Chart of Account structure is the most advanced in Managerial Cost Accounting. Supporting the Responsibility Accounting system, with detailed departmental operating accounts, introducing important re-allocation procedures and identifying basic functional activity accounts, this Managerial Accounting system will produce the very best reports.

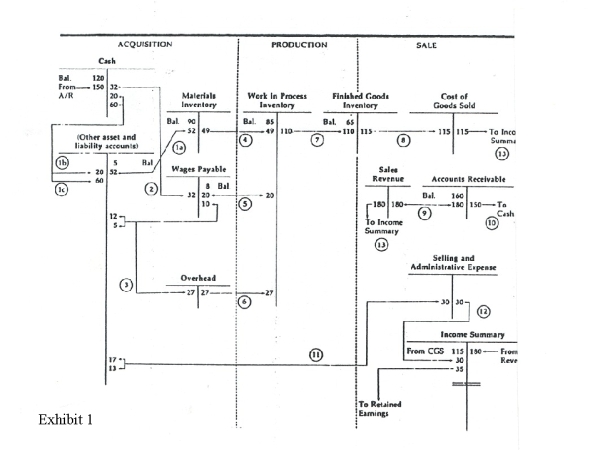

For you to better understand what we refer to as a separate Internal Accounting structure, let us first study the graphic shown in Professor R. Anthony's Cost accounting books. Exhibit 1 is a rare example, printed in a Cost Accounting book that shows the basic idea of having the production accounts separated from the financial accounts. We can see how Professor Anthony identifies the accounts to the left as those related to Acquisition. These are accounts that refer to Assets, Liabilities and Expense. But there are NO detailed expense accounts - because these accounts are included in the Overhead account. It is a mishap to have the expense accounts covered by an account called Overhead. In reality companies do not open Overhead accounts in their General Ledger - but have only accounts with expense denominations.

In this Exhibit we observe Sales accounts on the right, accounts referring to sales and administrative expenses, and also Asset accounts ( Accounts Receivable). This is an unpleasant mixture of accounts. In this presentation, notice that Professor Anthony has opened in the center of this exhibit, a group of accounts that he called "Production". Here is opened just a single production cost account, identified as the Work in Process Inventory account. Only the debit half of the Finished Goods Inventory account, is placed in this Production group of accounts, as if it should also belong to this group of accounts. What we learn from this presentation, is the important basic idea of dividing the total Chart of Accounts into three separate parts. Our Internal Accounting structure has just such a three-fold division of groups of accounts. However, we have developed a very detailed and precise configuration.

Let us analyze this next exhibit:

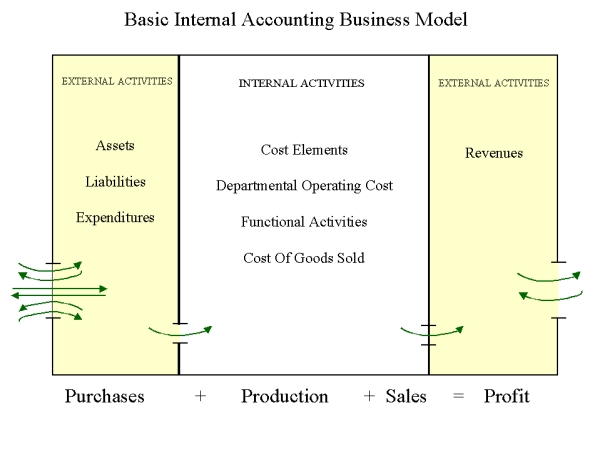

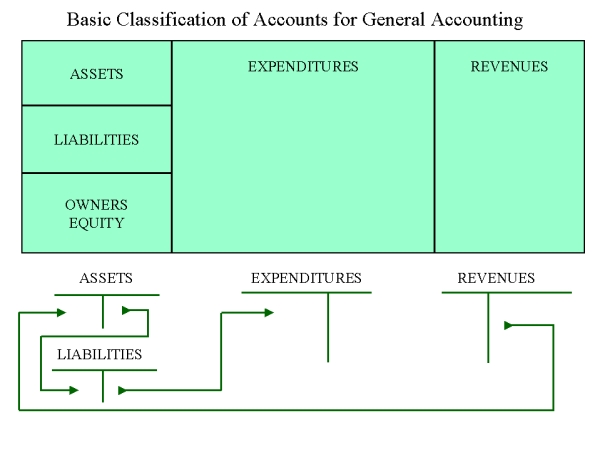

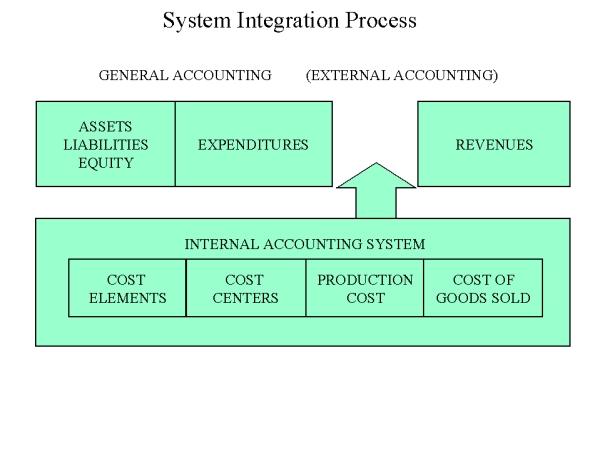

Exhibit 2 Here is the basic Managerial Accounting model. As if looking from above on the building, we see the outer walls and two internal walls, which divide the total structure of our company into three parts. The left part of this structure refers to the External Activities: we have a door in the wall through which our workers enter and their payments go out. Purchase material goes in, and payments go out. These transactions correspond to External Accounting - our Financial Accounting. The same type of structure with a wall to outer world, we have on the right side of this presentation. Through this door in the wall, our sold production (or service) is leaving our company and payments for these sales are coming in. Again, these transactions correspond to the External-Financial Accounting. Between these two parts we have structured a totally new perception: Internal Accounting: the Chart of Accounts for our Internal Managerial activities. Into these Internal Accounts will be entered amounts that correspond to this time period (accrual) and to the internal activities. From these Internal Accounts will be transfer amounts to Financial (External) Accounting (Such as finished goods inventory). These values per unit of production and in total, will show us the most accurate cost of our production or service. Internal Accounting must have a detailed structure of accounts, which will show us the following specific classes of accounts: 1. - Cost Elements 2. - Departmental Operating Cost 3. - Functional Activities 4. - Cost of Goods Sold Keep in mind the basic statement about activities registered in accounting: The activity of: Purchases + Production + Sales = Profit For purposes of discussion, we have prepared the next three graphics. The first is showing us the very well known structure of Financial Accounting.

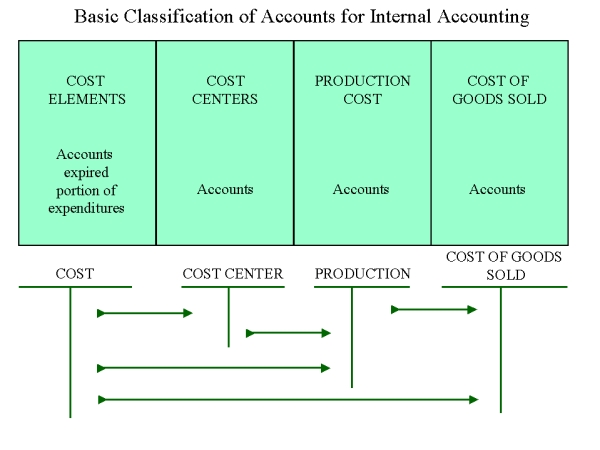

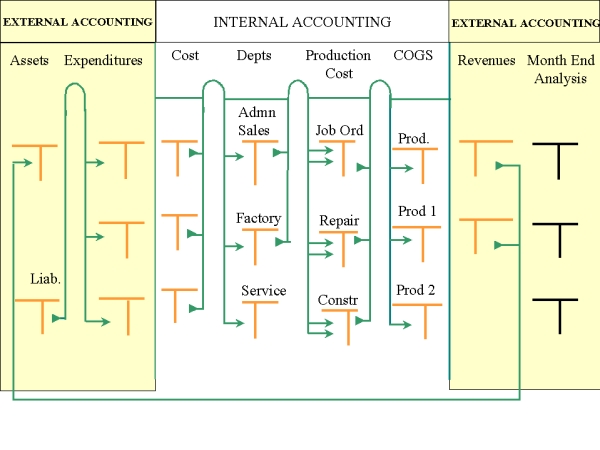

Exhibit 3: Notice the transactions are realized using the different T-accounts. These amounts normally move from Credit to Debit in the chosen accounts. This following graphic is much more interesting - it presents the basics for a separate Internal Accounting configuration.

The T-accounts are showing us, that from the Credit of the Cost Element accounts, we allocate these values to three different Classes of Accounts. First allocation will go to the debits of the Cost Centers Class of Accounts ( to the Department). Second allocation will be taken to the debits of the Production Cost Class Third allocation will be debited the Cost of Goods Sold Class of accounts. Here we discuss the basic rational of this allocation structure within Internal Accounting:

It is important to clearly memorize these basic allocation transactions as they corresponding to our Internal Accounting. The Reader will naturally understand that we will have many accounts in all these identified Classes. And there will be also transactions that at this present moment are not discussed. Please review the next graphic:

Exhibit 5. Her we see the basic idea of how to incorporate the Internal Chart of Accounts within the Financial Accounting structure. Let us go deeper into the analysis of this newly developed External and Internal structure. We suggest first to clarify basic details related to this new idea:

Exhibit 6: Here we have a relatively clear picture of the basic transactions flow within External and Internal Accounting. EXTERNAL ACCOUNTING : (not all shown on the exhibit) Transactions are commonly flowing from Credit of Liability accounts to the Debit of the Expenditures ( or Expense) or Assets accounts. From the credit side of our Revenue accounts the transactions flow to the debit of some Asset account. INTERNAL ACCOUNTING: We begin with the Cost Elements accounts. As we have debited our Expenditure (Expense) accounts with amounts that correspond to the External accounting, we will start our Internal accounting by crediting the Cost Element accounts. The total amounts recorded (credited) in these Cost Element accounts, must now be allocated to accounts where they belong. This question of where these amounts belong - can be explained in following way: Cost Elements are basically divided into following two groups:

All Indirect Cost - will be allocated directly to the Departments.These may be Administrative or Sales; Direct Production departments, Indirect Production departments or Service Departments. Let us now see the detailed graphic presentation of the Internal Accounting structure. This is the new Chart of Accounts for Managerial Accounting - presented graphically.

Exhibit 7 |