![]()

![]()

![]()

![]()

![]()

![]()

|

|

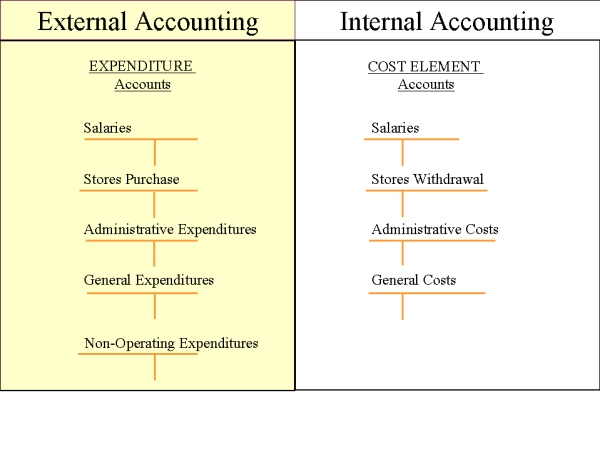

INTERNAL ACCOUNTING ENGINEERINGEXTERNAL AND INTERNAL LINKSHow do we LINK the External and the Internal accounting? That is: How are our External accounting Expenditure ( Expense ) accounts linked with our Internal Cost Element accounts. Let us study the following Exhibit 8, which will give us a simple answer:

Exhibit 8

In the EXTERNAL ACCOUNTING we debit our Expenditure ( Expense) accounts with the corresponding value of these expenses. These accounts belong to our External Accounting - just as we have learned in our Colleges and Universities. The credit to these accounts is registered in some Accounts Payable account ( our Vendor accounts, or those who are giving us services) or in the Cash-Bank accounts of our Assets. We may observe in this exhibit that there are total of 5 basic groups of Expenditure accounts - accounts that correspond to our normal business related transactions. Only one group of these Expenditure accounts - the last one - does not reflect some transactions that belong to some normal activity of our entity. This group is identified as Non-Operating Expenditures. In the INTERNAL ACCOUNTING we will start with the Cost Element accounts, which we have to credit. These Cost Element amounts correspond to the expired portion of our Expenditure (Expense) amounts. We are following the Matching Principle - accrual basis. These Cost Element accounts we have to credit - and debit some departmental account or some production cost account. Basically we have structured under Cost Elements the same groups of account, as we identified in the External Accounting. Some names of these groups differ. In the External Accounting we will have a group identified with the name Stores Purchase. In the Internal Accounting the corresponding group will be called Stores Withdrawal.

Exhibit 9 It is a logical consequence to have in the External Accounting under the Classification of Expenditure, accounts referring to the purchase value of raw material, parts and/or supplies. Within Internal Accounting, this group will refer to the amounts of raw material, parts and/or supplies that the company has withdrawn from the inventory to the production. In Internal Accounting, there is no need for the group called Non-Operating Expenditure. With this explanation, you will understand the simple relationship between the Expenditure accounts and the Cost Elements. The next Exhibit is referring to the same relationship between the External and Internal Accounting. Let us analyze this Exhibit.

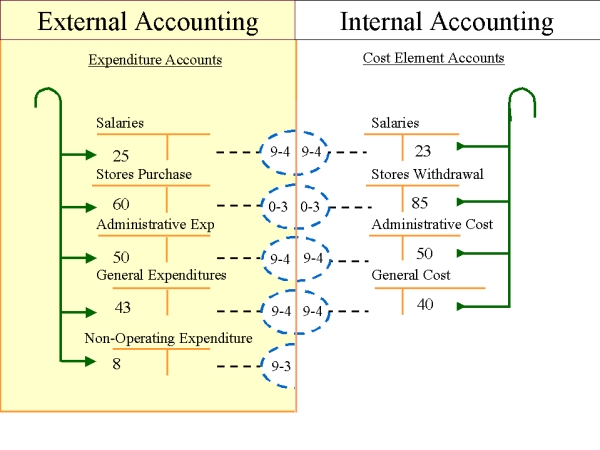

Exhibit 10 In this presentation, we have included some amounts registered in the debit of the Expenditure accounts and same or different amounts in the credit of the Cost Elements. We recommend that you analyze the differences between these amounts - and clarify why there are such differences. A special presentation in this Exhibit is showing us the month end closing transactions. As these are Temporary Accounts - they show us only the amounts that correspond just to this month-end (accounting period). We credit all our Expenditure accounts with the month end balance - and transfer these values to the corresponding account within the External Accounting. Here we will give you following information: Our Chart of Accounts, that is showing us both the External and Internal accounting structure, has a Class of accounts that we identify as: Results Analysis and Closing Accounts. Under this classification, we have there a group of accounts that compares the Expenditures of the month with the Cost Elements of the same period. This account code is: 9-4. That means: Class 9 and Group 4. Only the Stores Purchase account will be closed to an Asset accounts. This Group of Asset accounts, refer to the different inventories that our company has. Let us here clarify following procedure: As we have separated External and Internal accounting, in our Expenditure Class of Accounts we should also register all expenditures related to the purchase of raw material, parts, supplies etc. At the end of each month, we transfer the balance to the Permanent accounts registered under the Assets classification. MORE DETAILS ABOUT INTERNAL ACCOUNTING Let us now analyze some very important details about how the Internal Accounting has to be structured. We remember the basic recording transactions of the following accounting structure: Exhibit 11.

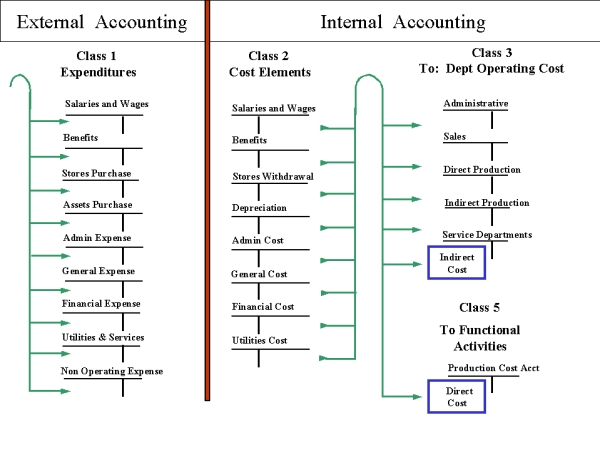

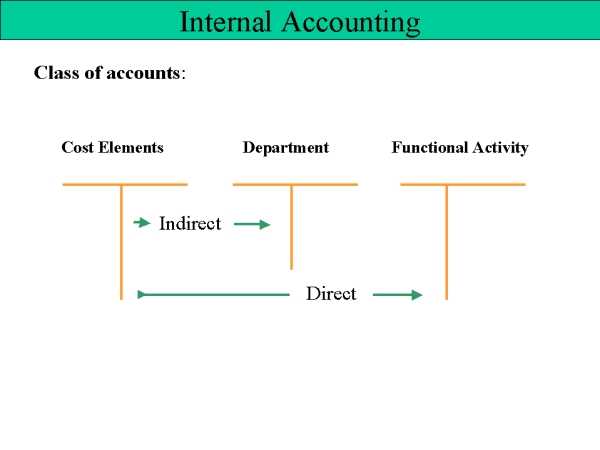

Internal accounting always begins with the COST ELEMENT accounts. These accounts represent and accumulate all accrued values for the accounting period. These amounts must correspond to the accounting period that we are working with, and refer to the companies activities of the same period ( month). Observe the two arrows moving from credit to debit of the Cost Element account in this Exhibit. The first arrow is taking all Indirect Cost to the different Departments of our company. The second arrow is taking all Direct Cost to the different Functional activities. Let us understand and remember this basic structure and rule. This next Exhibit reveals more details about this basic rule that we have mentioned.

Exhibit 12 The lines of the arrows are showing us how the amounts of the different Cost Elements are moving within the Internal Accounting. We remember that the Indirect Cost will be charged to the different Departments and the Direct Cost will be debited to the Functional Activities accounts and the Cost of Goods Sold will be taken from our Cost Element accounts to these accounts of goods sold. As you will correctly understand: The total amount in the credit of the Cost Element accounts must be the same as the total amount in the debits of the Departments plus the debit of the Functional Activities and the total debit of the Cost of Goods Sold accounts. Exhibit 13 reveals more details referring to these transactions.

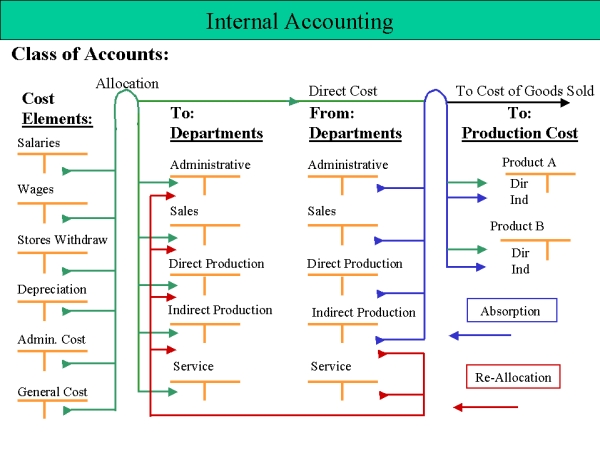

Exhibit 13 The new methodology in this exhibit requires the following terms: ALLOCATION = the transfer of the Cost Elements to the different departments, to the different Production Cost accounts and to the Cost of Goods Sold. RE-ALLOCATION = the transfer of the indirect Operating Cost of the different Indirect Production and Service departments to those department they have given their service. ABSORPTION = the transfer of Direct Production Departments Operating Cost to the different Production Cost accounts. The production will absorb these Departmental Operating cost - or we may say: The Departmental Operating cost are APPLIED to the different production cost accounts. This same approach will be used for the Departmental Operating cost of the Maintenance and Repair departments.

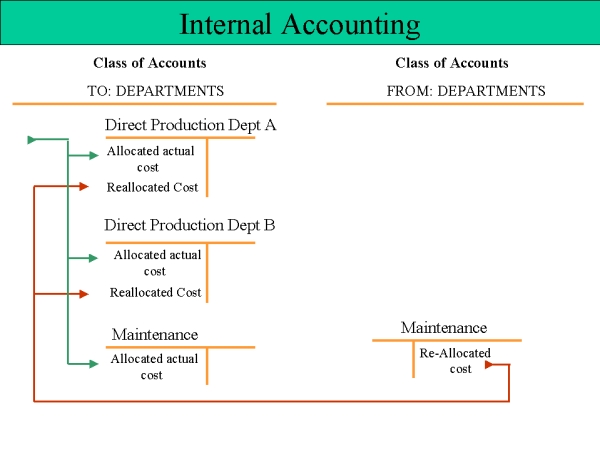

Referring to the question of the Re-Allocation of the Indirect Production Departments and Service Departments operating cost, the following exhibit shows how to proceed with this important Re-Allocation step.

Exhibit 14: This Re-Allocation procedure is highly important. Without this course of action, we would apply to the different Production Cost Accounts ONLY the Departmental Operating Cost of the Direct Production Department. Without this simple procedure we would ignore the need to apply to the Production Cost not only the Operating Cost of the Direct Production department but also the Operating Cost of the Indirect and Service Departments. These Indirect and Service Departments are giving their support to the Direct Production Departments - without this support, the Direct Production Departments would not be able to realize correctly their production activity. The management of the company agreed to establish these Indirect Production Departments (as Maintenance and Repair) and the Service Department (Janitorial, Security, Cafeteria) - with the purpose to serve these Direct Production Departments in their activity to fulfill their duties. The actual indirect Operating Cost of the Maintenance department, will be debited (charged) to the account established for this Maintenance department. The account of this Indirect Production Department was opened in Class 3 of the Internal Accounting Chart of Accounts. In Class 4 we must open the corresponding account of this Indirect Production Department - but instead of crediting these accounts with actual values, we credit this account with the pre-established budgeted amount of this department. From the credit of this Indirect Production Department account, we transfer the corresponding amounts to the different Departments to which this Indirect Production Department gave its service. This procedure is discussed in a different chapter of this web site. |