![]()

![]()

![]()

![]()

![]()

![]()

|

|

INTERNAL ACCOUNTING ENGINEERINGDIRECT LABOR RECORDING PROCEDUREIt is important for our understanding of Internal Accounting, that we recognize that the payment of hourly wage is also a Fixed Cost - just as we are referring to the Salary paid. As you will accept, the only difference between the Salary and the Wages - is the time period to which each payment refers. The company does not have any agreement to pay the worker less or more per hour, if the production increased or decreased per hour of work ( higher or lower efficiency). It is true, that we agreed not to charge to a smaller than normal production during a day, the total wages earned during this same day. That was the reason, why the accounting profession agreed to identify the Direct Labor payment as a variable cost, same way as the amount of Raw Material is used. However, you will have to accept, that the actual amount of Wages paid, must be recorded somewhere in our Internal Accounting system. The actual amount of Direct Labor Wage paid, should be charged to the Direct Production Department where the worker is assigned. This procedure will give management accurate information referring to its Responsibility Accounting System. In the budget of each Direct Production Department should be included the gross payment for the Direct Labor wages of the accounting period. In the following graphic, we identify the recording procedures in the traditional way, and with the Internal Accounting method.

Exhibit 15 In the traditional way - we credit the Accrued Payroll account with the grand total of the wages for the period. A part of this amount ( $ 5000 in our exhibit) will be charged to the Direct Production Department as indirect labor wages. Direct Labor wages will be taken directly to the debit of the Work in Process account, (terminology used in today's accounting). In our exhibit the amount of 39,000. If during this accounting period, we did not use all Direct Labor wages in the production process, because of some machine was out of service or for some other reason, we would have to debit the Work in Process account with some smaller amount, compared with the total value of $ 39,000. The difference between 39,000 and 36,000 ( as an example) we would need to debit to some specific account. We would need to create such special account. If we work with our new Internal Accounting - the total Accrued Payroll of wages would be taken directly to the Direct Production Department . We would need to specify in the departments information, how much would correspond to the Indirect Labor and how much to the Direct Labor. To: Factory Dept. - we have charged the actual value of Direct and Indirect Wages paid. From: Factory Dept. - we have to charge to the Production Cost Account only the amount of Direct Wages that correspond to the production of this time period. The difference will stay as a departmental operating cost

of this Direct Production This procedure is very important to remember - otherwise we would charge to the production a Direct Labor Wage that does not correspond to this production volume. The next two exhibits are related to the discussion of Direct Wages payments. Let us study them in detail.

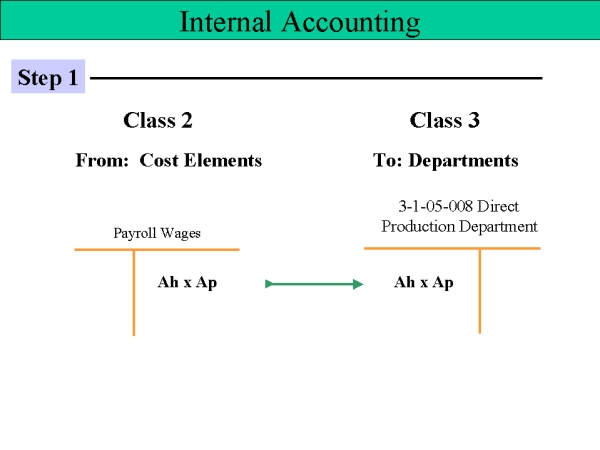

Exhibit 16 Step 1 - identifies the Class of Accounts that we use for this recording. Class 2 will have all Cost Elements accounts. This Class 2 is the very beginning of the Internal Accounting structure. We will credit Payroll Wages account with the Direct Payroll amount that we have received from the Payroll information - and this information refers to the Actual Hours worked (Ah) times the Actual Payment realized (AP), From credit of this Class 2 account -we will debit this amount to our Direct Production Departments in Class 3. This Class is identified with the name: To: Departments. This exhibit is also showing the possible departmental code that we could give this account. Now let us study the next exhibit:

Exhibit 17 The best way to express the production cost, is to charge to the Production Cost account the Standard amount of the corresponding Direct Labor Wages. As we have debited Class 3 Direct Production Department account with the amount that we have received by multiplying the Actual hours with Actual Payment ( Ah x Ap), we have to credit this Direct Production Department account in Class 4, with this same amount. However, we do not debit the production with the actual Direct Labor value. We express the Direct Labor Wages in STANDARD values. Based upon this requirement, we need to create within Class 4 From: Departments, two very specific accounts: First to show the Payment Variance and Second to show the Efficiency Variance. The Payment Variance account requires an accounting code that would correspond to the accounting code of the Direct Production Department. In our case, we could establish following code: 4-1-95-008. In same way, we would give the Efficiency Variance following code: 4-1-96-008. You will be able to understand the different amounts that we would transfer from Class 4 Direct Production department to the Payment Variance and to the Efficiency Variance accounts. The letter abbreviations are recorded in this exhibit. From the Efficiency Variance account - we transfer the Direct Labor Wage to the corresponding Production Cost account in Class 5. This Direct Labor Wage is now expressed in Standard hours and Standard Payment.

|