INTERNAL ACCOUNTING ENGINEERING

12. Transfer of Research, Internal Construction and Repair Cost

Internal Accounting can track costs down to the level of production-related activities, like Maintenance, Repair and internal Construction. Like production, these activities will be charged for materials, labor, and absorption costs. The resulting values could later be allocated back to Production job orders, or to a Managerial department.

Internal Accounting also supports linking a machine's

maintenance with specific activities; we can also use a certain base-line

(i.e., machine hours) to Re-absorb maintenance to specific Job-Orders.

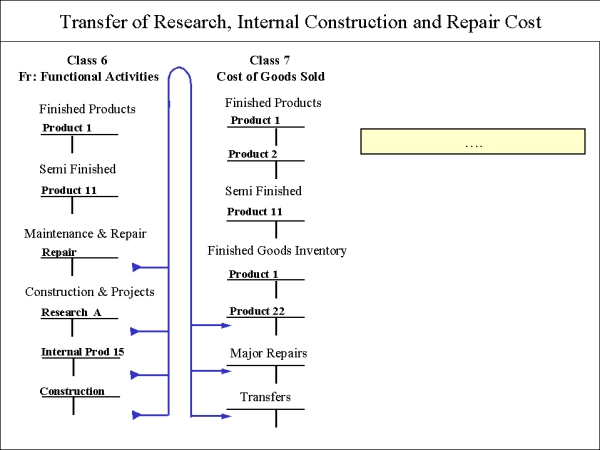

Transfer of Major Repairs, Research, Internal production and Construction projects from Class 6 to Class 7. Internal production and Construction may have to transfer their amounts at each month end to a Work-In-Process account in Other Assets. Other accounts transfer same amount as debited.

Internal production cost should all be tracked by Job-Order. This includes producing machines, tools, or building construction for internal use only. The Internal Accounting Structure has been used with great success in bridge and building construction projects. Main-accounts, Sub-accounts and special Sub-sub-accounts provided sufficient detail within each activity.

Repair and Construction Accounts

Major repairs are often recorded as Assets. These can be tracked with Job-Orders, like any other Functional Activity account. This is an Asset, even though it is not actually Inventory. It should be treated with its own contra-account for Assets tracking. At the end of each month this amount will have to be transferred to a corresponding External account in Assets. Repair-In-Process, or Repaired. Construction for Internal use only should be treated similarly. A Construction-in-Process account in Assets, can be tracked as another Functional Activity, on a monthly, quarterly and annual investment basis.

REPAIR COSTS

Production Cost Accounts refer to the production controlled by Job Orders, but also to Job Orders for repairs and production for internal use only.

Consider a two-month Repair Job Order. At the end of the first month, the total investment in the Job Order will equal Work-In-Process (because no amount was transferred from Class 6 to Class 7). At the end of the second month, when the Repair Job Order is completed, its total will be credited to an Internal Repair Cost Account (Class 6) and transferred to Finished Repairs (Class 7).

INTERNAL CONSTRUCTION COSTS

Internal construction is credited to Internal Construction Cost (Class 6) each month with the same amount charged to Production Costs (Class 5). Instead of a Work-in-Process account, a special "Construction in Progress" account in Assets should be opened. The construction amount invested this month is transferred from a Construction Cost Account (Class 6) to a Semi-finished-Construction account (Class 7).

From Class 7, we transfer the "Construction in Progress" value to an Assets account in Class 0. To this account we have to continue to add monthly amounts of investments in construction, and only when the project is finished, the total amount will be transferred to an Assets account.

Let's review the control of construction for internal use only. Production Cost Accounts can also have several Main-accounts to control internal production of tools, machines and buildings, and also Sub-accounts to track costs for specific items. Here is an example:

Construction is identified with Main-account of 5-7-40-000.

Main-account 40 can be divided into 9 different Main-accounts from 41 through 49. Main-account 41 can refer to, say, excavations. Within Main-account 41 we can open Sub-accounts to record separate excavation jobs. Here is the structure:

5-7-00-000 CONSTRUCTIONS

5-7-40-000 CONSTRUCTION # 4

5-7-41-000 EXCAVATIONS

5-7-41-010 Main building # 1

5-7-41-011 Excavations Consulting

5-7-41-012 Excavation Engineering

5-7-41-013 Excavation Machine lease

Maintenance, Repair and Internal Construction can be tracked as accurately as any Direct Production and any Job Order. That is the lesson of the Internal Cost Accounting System.

MACHINE LEASE OPTION

Internal Accounting provides an Internal Machine Lease option to help manage accounting of repairs over the lifetime of the machine.

The same point of view could be used for Airline Companies - where the plane would be 'leased' to fly different routes.

Internal Accounting can capture an daily or hourly machine operating rate, then lease this machine internally by that rate.

The actual operating cost, including purchase price, installation, space rent, depreciation, insurance, power,

interest, maintenance and repairs, can now be compared with a lease cost, and the computed rate can be fine-tuned every year.

This method is described in the Articles section of this web site under

"Machine Lease Agreement".