INTERNAL ACCOUNTING ENGINEERING

Inventory Transfers

13. Transfer Accounts

There are two very different kinds of Class 7 accounts, and so there are two different Class 7 rules:

|

Class 7 Cost of Goods sold accounts transfer their balances to Calculated Operating Profit (Class 9, Group 7), which corresponds exactly with an Income Summary Account. Compare sales costs with sales revenues. | |

|

All other Class 7 accounts transfer their balances to Asset accounts, since they are Contra accounts to Assets. They hold amounts prior to month-end, then transfer to a Balance account. Compare these amounts with budgets for true cost insights. |

INVENTORY Cost Accounting

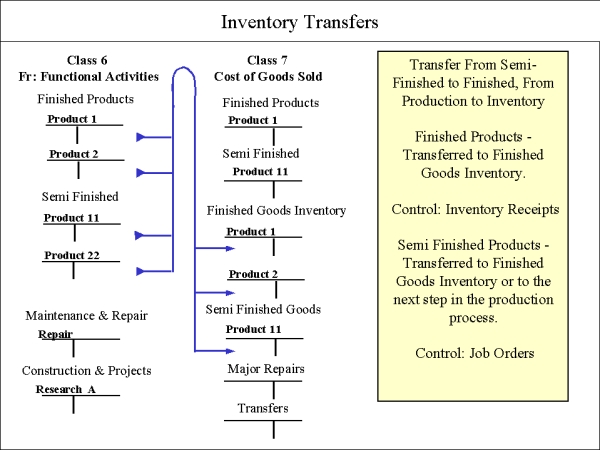

When production is completed for a Job Order, Product Costs (6-n) are charged to Finished Goods Inventory (7-n). Raw material costs, other direct variable costs, direct labor department costs, and absorbed indirect departmental costs are summarized in one sum. (Note: No Administration or Sales Costs are included at this point.)

Finished Goods Inventory is a contra-account to Financial accounting's Assets Inventory Finished Goods account. This contra-account shows beginning inventory debits and ending inventory credits, reflecting a monthly Income Statement. Like all balance accounts it is inactive until month-end closing.

Transfer Accounts also fall into this category. Transfer Accounts track internal transfers of goods. Branch sales offices often keep inventory storehouses, and so are a special type of Inventory account.

There are four kinds of Inventory accounts in Internal Accounting. (1) Finished Goods Inventory); (2) Semi-Finished Goods Inventory; (3) Repair and Construction Inventory and (4) Transfers.

Since Internal Accounting supports treating Repair and Construction projects like Production project, this implies setting up RIP and CIP accounts to carefully track these investments.

Inter-Company Transfers are handled as below:

1. Finished Goods Inventory Withdrawal (2-4) are charged to Transfer account (7-8). This is a Finished Goods Transfer to Branch Office transaction.

2. Month-end transfer transactions (7-8), are charged to Finished Goods Inventory Assets at that Branch Office account.

Use the same procedure when employees purchase finished goods, using (7-9): a Finished Goods Transfer to Employees account.

At month end, the Product Inventory accounts (7-n) transfer to Asset accounts, since they are Contra accounts to Assets.