INTERNAL ACCOUNTING ENGINEERING

15. Allocation of Inventory Transfer

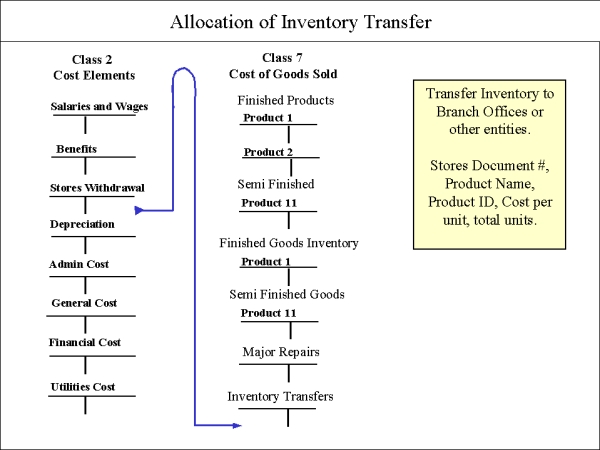

These are Inter-Company Transfers, or 'Inventory Moves' from one internal department to another. An example is a transfer of finished goods to a Branch Office. The first source document would be an inventory withdrawal (Credit Class 2 account of Finished Goods Inventory, and Debit a COGS Transfer Account (Class 7) The month end transaction would take the amount from credit COGS Transfers to debit the appropriate Branch-Office Inventory account.

TRANSFER ACCOUNTS

Class 7 contains two kinds of accounts: Cost of Goods Sold accounts and Inventory Group accounts, Contra Accounts to External Assets accounts.

Internal Accounting keeps the double entry procedure intact by refusing to credit Internal Accounting and debit External Accounting. In keeping with tradition, Internal Inventory accounts (including Major Repair and Construction accounts) are Contra Accounts until month-end closing.

Transfer Accounts also fall into this category. Transfer Accounts track internal transfers of goods. Branch sales offices often keep inventory storehouses, and so are a special type of Inventory account.

Inter-Company Transfers are handled as below:

1. Finished Goods Inventory Withdrawal (2-4) are charged to Transfer account (7-8). This is a Finished Goods Transfer to Branch Office transaction.

2. Month-end transfer transactions (7-8), are charged to Finished Goods Inventory Assets at that Branch Office account.

Use the same procedure when employees purchase finished goods,

using (7-9): a Finished Goods Transfer to Employees account.

Financial transactions still remain within External Accounting.

Stores Withdrawal: Product name, ID, cost per unit, total units, stores document #. Transfer from stores inventory to Branch Offices (or other entities); Material name, ID cost per unit, total units, stores document ID.