INTERNAL ACCOUNTING ENGINEERING

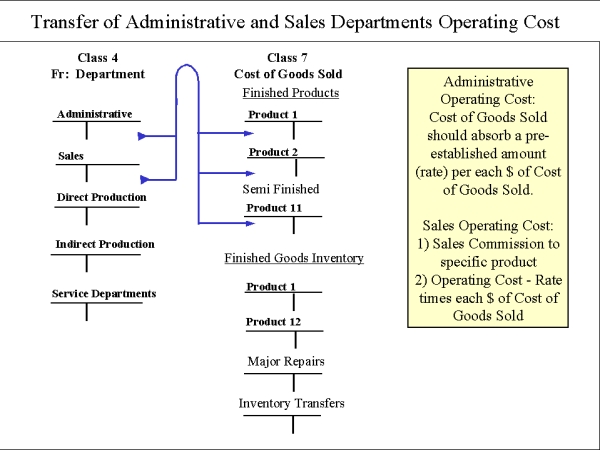

Transfer of Administrative and Sales Departments Operating Cost

16. Absorption of Administrative and Sales Costs

Standard calculated costs are recorded in Class 7 as Cost of Goods Sold, thus fulfilling the need to Matching Costs and Revenues. Internal Accounting, separated from External Accounting, provides the flexibility to finally complete this work rationally, logically, not only for production costs, but also for administrative and sales operating costs.

The Manufacturing Cost of each unit sold is a combination of raw material (Class 2), direct labor (Class 4BD), and absorbed indirect costs (Class 4CD). Now we must add to this Manufacturing Cost, all Administration and Sales Department Costs (Class 4AD).

Administration and Sales Department Costs should also be transferred to COGS (Class 7A). To do this, a standard absorption base is ideal, and any effort expended to design one is worthwhile. But even a simple base is sufficient in Internal Accounting to provide a reliable and practical report.

Administrative Departments include all general administrative units, but not administrators for production departments, such as supervisory units. They may include the Production Manager's Department. Sales Departments can include Raw-Material Inventory, Finished Goods Inventory, Purchasing and Delivery units.

Notice there are three kinds or Groups of COGS Accounts. To maintain standard double-entry procedures within Internal Accounting, we maintain three Groups of COGS accounts:

a) FINISHED GOODS INVENTORY Accounts Group

b) REPAIR AND CONSTRUCTION Accounts Group

c) TRANSFER Accounts Group