![]()

As we have explained in the very beginning of our presentation of this new Internal Accounting system, we have to separate the External-Financial Accounting from the Internal Managerial Accounting structure.

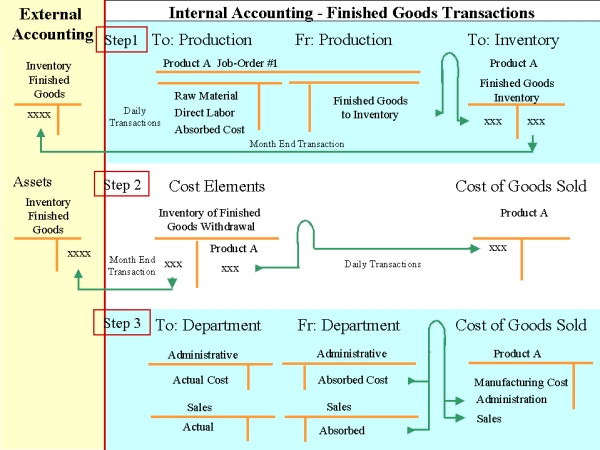

The Inventory of Direct Material is recorded as an Asset of our Company. It belongs to the External accounting. The conversion of this Direct Material combined with the Direct Labor is realized in our Internal Accounting. When the product is finished, it will be credited the corresponding Production account in Class 6, and transferred to the account in Class 7, that will correspond to the Inventory of Finished goods. Here the amount will be kept to end of the accounting period ( month), when it will be taken during the month end transaction to the Inventory of Finished Goods in the Assets. This presentation is shown in this following Exhibit:

Exhibit 34

Step 2 in this Exhibit is showing how we take the finished goods out of the Inventory [ using Class 2 account ] and allocate it to the debit of the Cost of Goods Sold account in Class 7.

The Step 3 - is illustrating how the Administrative and Sales departments will apply their departmental operating cost to the account of Cost of Goods Sold. From Class 4 - From Departments, these costs are applied to the accounts in Class 7, the Cost of Goods Sold.

![]()

Stores Inventory:

A key factor in Variance Reporting is Stores Inventory data. There are three kinds of Stores Withdrawals: Supplies withdrawals for Departments, Raw Materials withdrawals for Production, and Inventory withdrawals for Sales.

For Price Variance reports we focus upon Raw Materials withdrawals. If we withdraw something from Stores this month, there is no guarantee it will have the same Actual cost as last month. It may vary from our Budgeted, Standard costs. The monthly variance can be measured by reporting Stores data.

PURCHASE PRICE VARIANCE: Purchase Price Variances will report the actual cost of materials withdrawn for the month compared with a Budget.

* Price Variances (for expired portion of expenditure only) compare Standard (budgeted) prices vs. Vendor Invoice prices. The stores withdrawal algorithm is:

Price Variance 2-3-01-005 (Aq*Ap) - (Aq*Sp) where Aq is Actual Quantity, Ap is Actual Price, and Sp is Standard Price.

Stores Inventory Sub-accounts provide exceptionally valuable information for management.

Exhibit 35 shows a traditional inventory account.a) A single Assets Inventory Stores account contains the Beginning Balance.

b) All purchases and all raw-material-returns are added to the debit column of the Beginning Balance.

c) All withdrawals and all sales returns are added to the credit column of the Beginning Balance account.

d) Cycle Counts for Raw Material Inventory will adjust Inventory regularly.

The Ending Balance account is calculated at month-end. All inventory stores transactions are always related to this account, no matter what application of GAAP is employed.

Exhibit 35

This next Exhibit shows how the Internal Cost Accounting System breaks down this account into multiple transactions:

Exhibit 36

Purchase Accounts:

Purchase is an Expenditure (Class 1), debited to Stores Purchase. A Stores Withdrawal (Class 2) is the expired portion of the expenditure for this Stores Purchase. That is the key to Internal Cost Accounting.

Every purchase in an Expenditure. Some purchases are Assets. Some purchases are Costs. In a traditional system raw material purchases accumulate directly into an Asset account (by crediting A/P (Class 0), and debiting Assets, Stores Inventory (Class 1)).

Internal Cost Accounting logic for Stores Inventory accounts follows:

a) All purchases are debited to Expenditures, Stores Purchase (Class 1).

b) Return to Vendor returns are credited to Stores Purchase.

The corresponding debit is registered in A/P. This Stores Purchase is a typical 'pure' account.

.Material Withdrawals.

Internal Accounting tracks all source documents for all Stores Withdrawals.

Raw material withdrawn from inventory for production, or for any other use is a credit to Stores Withdrawal (Class 2), a classic example of an 'expired portion of Expenditure.'

Crediting Stores Withdrawal (Class 2), the raw material amount is debited to a Production Cost account (Class 5). All other types of withdrawal will be debited to some department or to some functional activity account.

Material returns to Inventory will be credited to Class 5 and debited Class 2.

Finished Goods Transfer.

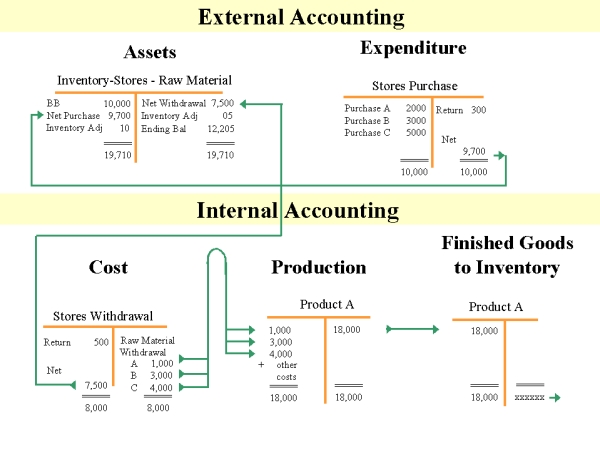

Exhibit 37 shows a Job-order (referring to product A), begun and finished in the same month. The Job-order includes a record of raw-material costs (Class 6) in its transfer to Finished Goods Inventory (Class 7).

At month-end, the balance of Withdrawals and Finished Goods Inventory are transferred to a corresponding Asset Inventory account.

Exhibit 37

Simplification of Inventory Stores.

To balance raw materials Stores Withdrawals (Class 2) at month-end, we debit this account with the total withdrawal amount , and credit the Asset Inventory Stores account (Class 0).

This maintains pure accounts and controls total purchases and total withdrawals. At the same time, this also simplifies Inventory Stores accounting.

Exhibit 37 also shows the Finished Goods Inventory contra-account

transferring its balance (Class 7) to External Accounting's Finished Goods Inventory account (Class 0) at month-end.

Only at month-end do we transfer Inventory Stores account to Assets. The beginning balance of Assets is simply the previous-month's closing balance. This monthly figure clarifies net purchases and withdrawals.

(Inventory adjustments are recorded in Asset accounts ad hoc, because they are literally Asset adjustments.)

Sales Transactions

Each sale is accompanied by some stores withdrawal source document or other. Internal Accounting sales transactions are credited to Stores Withdrawal of Finished Goods (Class 2), and debited (allocated) to Cost of Goods Sold (Class 7).

At month end sales transactions are handled like raw material transactions, debit the net amount of Finished Goods Withdrawal (Class 2), and credit the Inventory account in Assets (Class 0).